Introduction

The mass affluent—households with income-producing assets (excluding a primary residence) worth between $100,000 to $1 million—control an estimated $10.2 trillion in wealth. Incumbent management firms have traditionally focused on high-net-worth clients, but the mass affluent market has become too big to ignore.

But the clock is ticking. A wide range of competitors are vying for a share of this market, from digital startups, robo-driven investment services, and low-cost trading platforms to blue-chip incumbents like Goldman Sachs. But success will elude those who stick to business as usual. Today’s disruptive markets demand transformational strategies—and the infrastructure to support them.

Mass affluent investors want and increasingly expect personalized investment services. However, wealth managers can’t deliver the same service levels they offer to high-net-worth individuals.

As past experience has shown, that is not economically viable. Instead, firms must leverage automation, digitization, and analytics to deliver personalized, but largely self-service-driven, experiences that approach the high-touch offers reserved for high-net-worth clients.

Unfortunately, that is almost impossible with the traditional application-building environments and the disparate IT systems that support them. Development takes too long. It is too cumbersome to stitch together disconnected systems. And at the end of the day, firms end up delivering disconnected customer experiences.

Experience has also shown that a 12-to-24 month, bottom-up digital transformation project won’t solve the problem. They require massive upfront costs and significant project risk. And businesses end up with a solution that, in the age of disruption, is often out of date by the time it comes online.

So what is the answer? Unqork’s Codeless as a Service platform can close the gap. They enable you to accelerate application development, thanks to an all-visual building environment. Platforms like Unqork are also designed to seamlessly connect customer-facing applications with backend and third-party systems. Only in this way can businesses deliver unified customer experience across offerings, while simultaneously driving down IT and account servicing costs. Since enterprise-grade security and compliance can be deeply embedded in the DNA of a the Unqork platform, they can act quickly and confidently to unlock the enormous opportunity that the mass affluent market offers.

JPMorgan Chase's Guddu Money, Head of Process Engineering, Asset and Wealth Management, on CaaS

The opportunity

In the US alone, there are an estimated 35 million mass affluent households that, together, own roughly 37% of America’s liquid financial assets. Mobile-first businesses like SoFi and Acorns are making inroads, but established incumbent firms are in a particularly good position to dominate this market.

The mass affluent demographic still skews older, with two-thirds over 55 years old. This gives larger incumbents an advantage, since this demographic tends to value established brands.

Larger established firms are also in a better position to offer a comprehensive range of financial services, a key advantage among the mass affluent. According to a recent study by Cerulli Associates, half of all affluent investors (49%) would prefer a single company to serve most of their financial needs. That number rises to 66% for investors under the age of 30.Regardless of if you build an application in a matter of months or days, or if it’s internal- or external-facing, or if it’s a greenfield application or an extension of an existing one, you can be assured that all assets will adhere to visual guidelines and require little-to-no intermediation from a brand designer.

Who are the mass affluent?

While definitions vary, the mass affluent can generally be defined as members of households controlling income-producing liquid assets ranging from $100,000 to $1 million. Here are some key characteristics of this demographic:

- Most are over 55. According to Nielsen, baby boomers make up 41% of the mass affluent segment, while Gen Xers and millennials account for 37% and 9% respectively.

- But millennials are catching up. The number of millennials entering the ranks of the mass affluent will massively accelerate in the next two decades because of what Cerulli Associates calls the Great Wealth Transfer, as Gens X and Y inherit an estimated $68 trillion from their elders.

- They’re digitally savvy, but there’s a generation gap. The mass affluent “have a strong online presence,” according to Nielsen, but it is not equally distributed. About three in four (73%) of affluent boomers own a smartphone, versus 93% of millennials. Both, however, outpace the general population (71%).

A high income doesn’t equal affluence. Curiously, income and investment wealth are not directly correlated. Only about half of households with $100K-plus annual income own income-producing assets (IPA) worth $100K-plus. Yet, among those with over $100K IPA, only about half have $100K or more household income, according to Nielsen.

The competitive landscape

From digital startups to traditional incumbents, the wealth management industry clearly has its sights trained on the mass affluent market. The boom has been led in particular by the advent of “robo-advisors,” which use algorithms and advanced software to build and manage an investment portfolio by asking relatively simple questions about the investor and their financial goals.

To compete in this increasingly crowded market, leading industry analysts suggest adopting the following strategies:

- Digitize high-touch services. As new technologies such as AI and Big Data reach maturity, firms are able to provide highly personalized investor experiences on a purely digital basis, enabling “wealth managers to serve mass affluent clients with solutions historically only available to high net worth investors,” write Deloitte analysts in Retooling Wealth Management for the Digital Age. According to Deloitte, all investor demographics “are ready for digital capabilities in some way, shape, and form.” And as Gens Y and Z join the ranks of the mass affluent, a strong digital strategy will become increasingly vital to future growth.

- Integrate offerings on a single platform. Both to serve customers more seamlessly and to drive down servicing costs, firms should work to build and connect a comprehensive set of offerings on a single platform. “An integrated platform can translate into more cost-efficient delivery and an improved experience for the mass affluent client,” argue Celent analysts.

- Accelerate development timelines. Market disruption is the new norm, and wealth management firms can’t afford to spend a year building a new digital offering, or months to tweak and/or enhance it. That is why Accenture analysts urge wealth management firms to “set up the business in a modular way to identify, analyze and act immediately on changes in the market and client expectations.”

Unfortunately, firms have faced serious technological challenges in achieving all these goals simultaneously. In a recent Thomson Reuters survey, 68% of managers said that “learning about and keeping up with technology” was the top challenge they face. Only 27% of respondents “currently have—and are happy with—their mobile platform.”

Tech roadblocks to serving the mass affluent

Personalization and automation were once opposed terms. But in the age of process automation, AI, and Big Data analytics, you can deliver both at once. And that is exactly what the mass affluent market demands. To achieve this, you need to:

- Digitize and automate slow, manual processes

- Provide rich, intuitive, ubiquitous self-service functionality

- Personalize offerings and guidance intelligently via sophisticated algorithms, AI, etc.

In their digitization efforts, wealth management regularly face the following technological roadblocks:

1. Disconnected systems and customer experiences

To serve customers efficiently, investment accounts must integrate with a wide range of both customer-facing and backend systems. However, many wealth management firms, facing sudden market disruptions, have built new digital offerings on an ad-hoc basis.

Too often, this approach results in costly account servicing, disconnected experiences, and/or expensive integration efforts—and sometimes, all of three at once.

2. Long, costly, and risk-prone digital transformation projects

To overcome the drag of disconnected systems and slow development timeframes, some financial institutions have embarked on one- to two-year digital transformation efforts. The problem is, this approach is expensive and disruptive, and also involves a high level of risk. Surveys reveal that 85% of such projects go over schedule, and 70% of large-scale digital IT programs fail to reach their stated goals.

3. Lack of skilled technology resources

The traditional approach to digital innovation has required a range of rare, expensive technology resources—and many companies find they simply can’t find the necessary resources. Some 74% of enterprises have a digital strategy in place, according to a study by Forrester, yet only 15% seem to have the right skills to deliver it.

4. Security and compliance vulnerabilities

By definition, investment applications must handle sensitive data and personally identifiable information. That can make a single data breach a devastating event. Yet application codebases have grown so large and complex, it is not surprising that the code hides 82% of identified web application vulnerabilities.

Meeting the challenges with a CaaS platform

With a Codeless as a Service platform like Unqork, you can overcome the challenges that have long stymied digital transformation efforts.

1. Accelerate development 3x faster.

Studies have found that the average enterprise solution can take up to a year to go from ideation to production. With a completely visual, CaaS platform, development cycles are greatly accelerated. According to James McGlennon, CIO of Liberty Mutual, Unqork has proven “a minimum of three times faster and three times less expensive” than the company’s previous approach. Wealth managers have been known to build a solution in just a few weeks, and even a few days in some instances.

2. Plug-and-play systems integrations

With visually configured APIs, a CaaS platform like Unqork enables developers to connect to backend, customer-facing and third-party systems via any modern API—all using a fully configurable visual interface. To support transactional resilience, Unqork also makes it easy to apply asynchronous integration and custom scheduling of data interaction. Finally, it speeds and simplifies data loading via legacy protocols or legacy web services.

3. Empowered citizen developers

Modern programming languages can take a year or more to learn. By contrast, it is possible to start developing on a visual-based CaaS platform like Unqork in a matter of weeks. The platform handles so much of the heavy lifting that you can entrust routine tasks to less-experienced developers—Unqork calls them “Creators.” You can redeploy senior developers to more strategic, value-add activities, since the platform ensures that all the elements work together seamlessly and securely. In fact, the Unqork platform reduces bugs by up to 600x—a major boost to productivity, since professional coders typically spend up to 75% of their time locating and squashing bugs.

4. Security & compliance

With a platform like Unqork, all elements are rigorously tested for security and compliance vulnerabilities. Creators simply apply the feature repeatedly without risk of creating new vulnerabilities. Unqork solutions are also powered by up-to-date regulatory and enterprise rules engines for complex regulatory requirements, including SOC2, FATCA, CRS, UK CDOT, Dodd-Frank, EMIR, and MiFID II. The same principle holds for security features, including native encryption of data (both in transit and rest), custom RBAC capabilities, and crowd-sourced penetration testing.

The wealth management lifecycle on a CaaS foundation

When you are able to build a robust, secure application in a matter of weeks, the ways you can serve the needs of mass affluent investors are limitless. You are also in a position to remain resilient in the face of whatever next big disruptor looms on the horizon. With that in mind, let’s consider how a CaaS platform can quickly transform four essential steps of the wealth management lifecycle.

1. Digitized customer onboarding

Instead of manual, paper-based processes, a CaaS solution like Unqork’s Client Onboarding offering enables new customers to provide critical information via digital channels and on a self-service basis. Besides providing a seamless experience that encourage prospects to become customers, you can also easily layer business intelligence into the process, for example:

- Customizing experiences based on triggers such as sales channel, region, client preferences, products, and regulations.

- Understanding client risk tolerance with a configurable suitability engine that also meets regulatory requirements.

- Enhancing cross-sell with analytics for customer behavior and preferences.

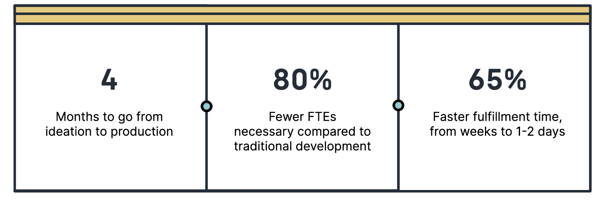

Success Story

A top-5 wealth manager was saddled with expensive, high-touch processes for onboarding and servicing clients, which led to high costs and lowered advisor productivity. Seeking to create a richer client experience and digitize enterprise-wide operations, the firm used Unqork to develop an end-to-end digital solution for 12,000 financial advisors across 350 branch locations. The solution enabled next-generation advisor workstation capabilities, streamlined onboarding & maintenance, and enabled scalable back-office capabilities (e.g., ACATs). The solution is fully integrated with the manager’s existing record-keeping systems, as well as third-party services such as SFDC, Docusign, and PLAID.

2. Highly efficient account maintenance

At many firms, basic tasks like changes of address, withdrawals, and transfers involve forms, faxes, and time on the phone speaking to an advisor—low-value activities for clients and advisors alike. With a solution like Unqork’s Account Maintenance offering, you can:

- Digitize account changes, AML/KYC, and transaction monitoring.

- Avoid lengthy “off-the-shelf” customizations and ad-hoc development.

- Detect anomalies with integrated analytics.

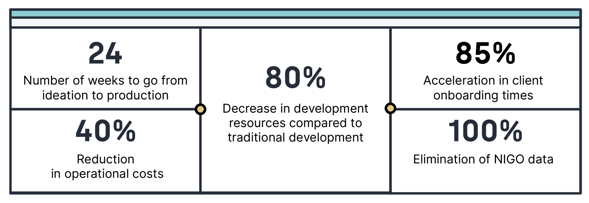

Success story

A leading global wealth management firm was looking to digitize the sales and servicing of their wealth products. With Unqork, the firm gained an end-to-end, multilingual application that incorporated suitability, investment selection, account opening, KYC, funding, and servicing. Ultimately, their revenue grew faster while their operational costs lowered.

3. A solutions marketplace

From basic portfolio management to life insurance and retirement products, today’s mass affluent clients prefer to minimize the number of firms with whom they do business. With a no-code solution like Unqork’s Solutions Marketplace offering, you can quickly and easily expand offerings via seamless integrations with proprietary and/or trusted third-party offerings into a centralized hub. As a result, you can:

- Easily onboard new clients through a single online channel.

- Automate manual compliance, suitability, and operational processes.

- Reduce time-to-completion by moving carrier/asset manager data collection onto the platform.

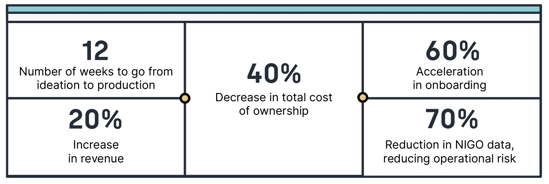

Success Story

A top-5 financial institution required bespoke relationships with insurance carriers, due to high-touch, manual processes. By partnering with Unqork, the company developed a direct-to- consumer, end-to-end fulfillment platform for advisors and clients across financial products (e.g., life, annuities, and retirement).